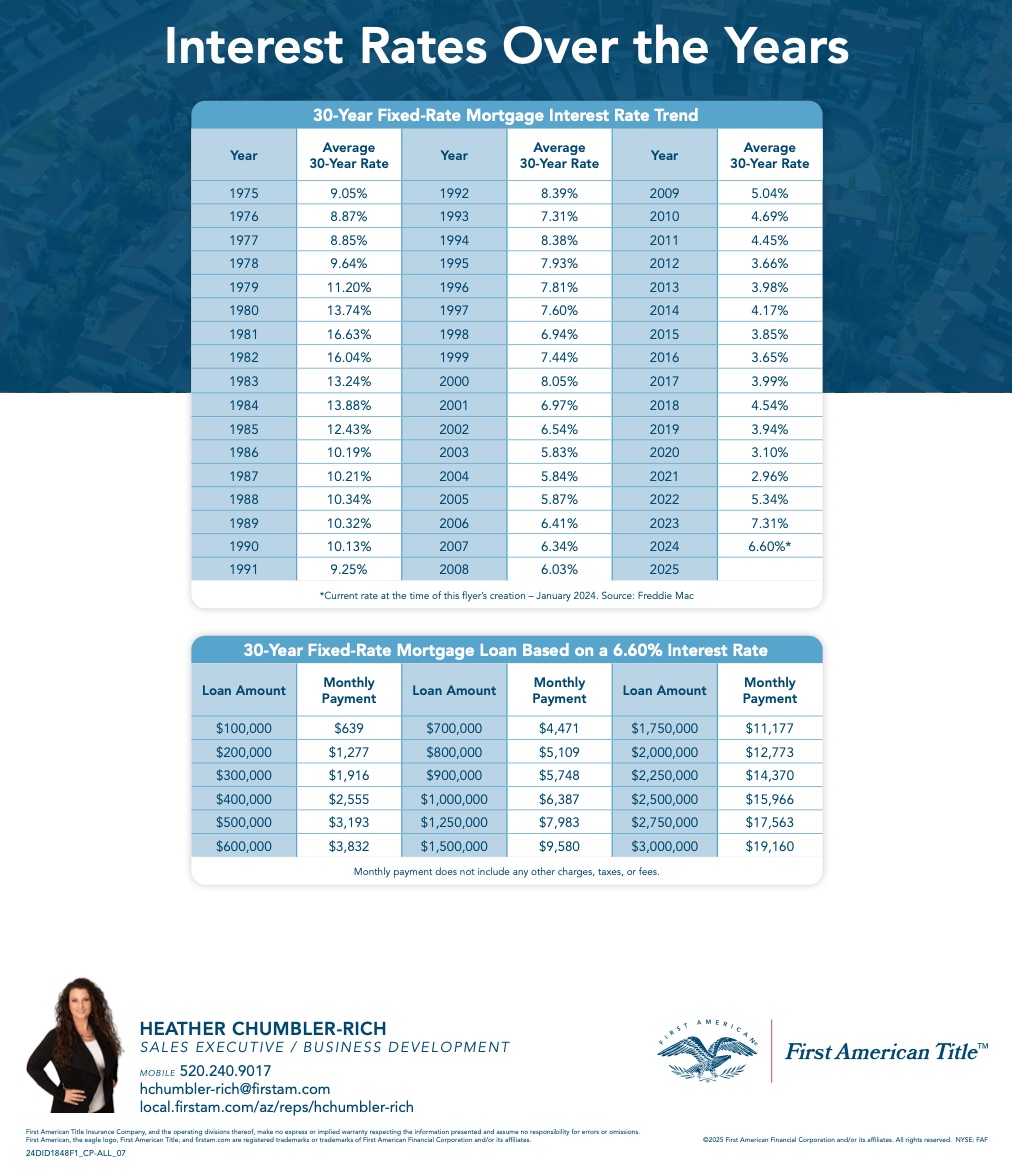

50 Years of Mortgage Rates and What It Means for You!

📊 From sky-high peaks in the 1980s—when rates soared above 18%—to historic lows below 3% in recent years, the housing market has seen it all. But what do these numbers mean for you?

🔹 Today’s Rates Are Still Favorable

While current mortgage rates are higher than the rock-bottom lows of 2021, they remain much lower than the double-digit rates of the past. Borrowers today still have opportunities to secure a mortgage at historically reasonable levels.

🔹 What Drives Mortgage Rates?

Rates fluctuate based on inflation, Federal Reserve policies, and the overall economy. When inflation rises, mortgage rates typically follow. When the economy slows, rates often decrease to encourage borrowing.

🔹 Should You Buy Now?

Timing the market is tough, but homeownership remains one of the best ways to build long-term wealth. If you find a home you love and can afford the monthly payments, it may still be a smart move—even if rates aren’t at record lows. Plus, refinancing later is always an option if rates drop!

🔹 Key Takeaway

Mortgage rates rise and fall, but homeownership continues to be a powerful investment in your future. Stay informed, be patient, and make decisions based on what’s best for your personal finances—not just the numbers on a chart.

Here are 3 key strategies to help you master the ups and downs of mortgage rate cycles:

🔑 1. Understand the Economic Drivers

Why it matters: Mortgage rates are closely tied to broader economic trends—especially inflation, Federal Reserve interest rate decisions, and job market strength.

What to do:

- Follow simple financial news (or summaries) to understand when inflation is rising or falling.

- Pay attention to the Federal Reserve’s actions—when they raise rates, mortgage rates usually climb too.

- Use tools like mortgage rate forecasts to stay ahead of trends.

🔑 2. Time Your Actions, Not the Market

Why it matters: Trying to perfectly time mortgage rates is nearly impossible—but smart timing of your decisions can still save money.

What to do:

- Lock in your rate when it feels comfortable, especially if rates are rising.

- Consider buying when home prices dip—even if rates are a bit higher—because you can refinance later.

- Use pre-approval to hold a rate while you shop.

🔑 3. Refinance Strategically

Why it matters: You’re not stuck with your initial mortgage rate forever.

What to do:

- Watch for a 1% or more drop in rates as a signal to consider refinancing.

- Calculate your break-even point (how long it takes to recover refinance costs).

- Use refinancing to shorten your term, lower your monthly payment, or pull cash for major goals.

For a great primer, check out the National Association of Realtors® Consumer Guide to Mortgages and Financing below:

Pro Tip:

Keep an eye on rates, explore your options, and take the first step toward your dream home! By staying informed, acting smartly, and being flexible, you can ride the wave of mortgage rate changes like a pro! 🏄♂️💰

#MortgageRates #HomeBuying #FinanceTips

If you are in the market for buying or selling in Tucson, please explore my website for lengthy articles on real estate topics, buyer’s agent service details, seller’s agent service details, as well as helpful Tucson community links and information.